On October 29th 2020, the 19th Central Committee of the China Communist Party concluded its semi-annual plenum. The issue of discussion was to review the outline for the country’s 14th Five-Year Plan (FYP), the state’s vision of economic and social policy over the next five years. The 14th FYP, which will be released in March 2021, aims to improve market efficiency and self-reliance, and emphasise R&D and technological innovation. Perhaps most importantly, however, the plan will radically expand the pilot programmes of China ’s ambitious carbon trading scheme to a national level.

—

Since October 2011, carbon trading schemes have been implemented in eight jurisdictions across China. The pilot programmes were intended to test how these schemes would work under different conditions. Locations of pilot programmes include the political and business hubs of Beijing and Shanghai, the heartland of China’s manufacturing industry in Guangdong province and the densely populated industrial municipalities of Tianjin and Chongqing.

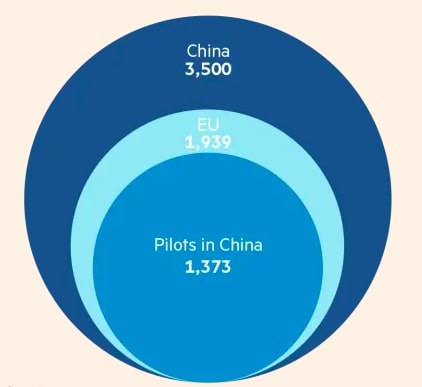

The pilot programmes appear to have been successful in reducing China’s carbon intensity, a measure of emission reductions calculated relative to economic growth and GDP, which fell by 48.1% in 2019 compared to a 2005 baseline. By the end of August 2020, China’s pilot carbon trading markets had a total carbon emission trading quota of 406 million tonnes of carbon dioxide equivalent, equal to around 9.28 trillion Chinese RMB.

China has therefore moved towards adapting the scheme to a national level, where it would become the world’s largest carbon trading market. The emphasis on the scheme in the 14th FYP indicates that it will be rolled out nationally within the next five years, although the specific dates and targets will not be known until the final draft of the plan is approved next March. As the US retreats from international commitments to mitigate climate change, China continues to position itself as a global leader in this regard.

You might also like: Climate Financing for Developing Countries Rose 11% in 2018- Report

There have been some challenges in implementing the national scheme, including multiple delays, bureaucratic reshuffling and concerns over transparency and accuracy of emission data.

The national implementation of the scheme represents the efficient strengths of the collectivist and growth-driven perspective on policy shared by China’s leaders, as well as the Chinese state’s shift towards adopting market-based solutions to combat climate change. The scheme’s implementation has, however, encountered resistance in the shape of China’s intricate bureaucracy, and policymakers will have to evaluate how to integrate its tried and tested top-down economic planning mechanisms with the national scheme’s market-based approach.

What are China’s Plans to Mitigate Emissions?

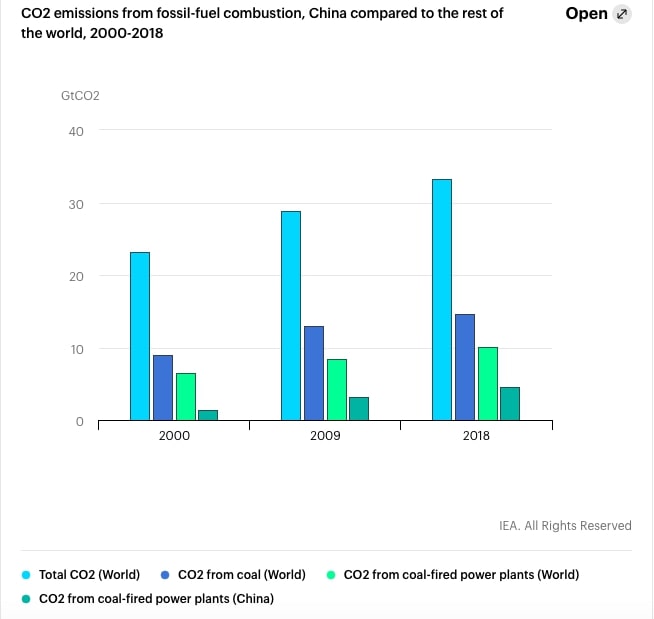

China has pledged to reach peak emissions by 2030, potentially as early as 2027, and will source 20% of its energy from low-carbon sources in 2030. To achieve these targets, China will reduce its carbon intensity rates by 60-65% by 2030, and will increasingly limit its reliance on coal-derived energy, which in 2019 accounted for a heavy 57.7% of its energy mix.

Discussing the national carbon trading scheme’s role in these targets, Ma Jun, director of the Institute for Public and Environmental Affairs, stated that: “The actions of rolling out the national carbon trading scheme cannot be postponed, otherwise, China will be unable to meet the goals of carbon reduction,” underlining the scheme’s importance to the country’s leaders. With a view towards adopting more market-oriented solutions to climate change such as carbon trading, Chinese economic policymakers have shifted from a command-and-control administrative style to adopting market-oriented solutions to tackle climate change.

Authorities will rely on market dynamics to regulate the scheme. A free market environment occasionally regulated by the state should ensure that rates of emission reduction will occur in the most cost-effective manner possible, as emitting entities can be more flexible in deciding when to lower emissions and when to trade emission allowances. Market forces will also take charge in establishing the allocation of resources and allowances.

Chinese policymakers have cooperated with advisors from jurisdictions where carbon trading systems have already been implemented, specifically the EU, Australia and California. There are some similarities between China’s scheme and the models operating in Western countries; for instance, the Chinese scheme’s MRV (monitoring, reporting and verification) strategies, certain target determination procedures and a preliminary focus on mitigating energy sector emissions are similar to existing policies in the EU trading scheme.

Once China’s national scheme becomes operational, 25% of the world’s emissions and nearly 50% of global GDP will be covered by a carbon market.

China has set up its national carbon trading scheme to operate in incremental stages, gradually unfolding to involve more sectors, and focusing on carbon intensity reduction targets. The pilot programmes have been useful in evaluating how a carbon trading scheme functions across diverse sectors. Overall, the scheme will cover emitting firms operating within eight sectors: oil, chemicals, construction materials, steel, nonferrous metals, papermaking, electric power and shipping. The first stage will tackle the energy sector, specifically aiming to use market forces to wean the country off power derived from inefficient coal-fired plants.

While the energy sector phase of the national scheme had most recently been slated to roll out by the end of 2020, it appears that the Covid-19 pandemic and its economic impact have pushed the programme back indefinitely, due to pauses in economic activity and difficulties in collecting and verifying emissions data. However, the scheme’s prominent inclusion in the 14th FYP indicates it remains a priority and that the energy sector phase will be rolled out over the next five years.

Carbon Trading in China’s Energy Sector

Tackling energy sector emissions will be critical to the scheme’s long-term feasibility. Coal continues to dominate China’s energy mix, and successful implementation of a national trading scheme in the coal sector will pave the way for future transitions.

For the first phase of the national scheme, policymakers do not appear to be imposing a hard cap on emission rates, as the focus remains on carbon intensity reductions rather than reducing absolute emissions. Each power company will have an individual carbon intensity benchmark based on their emissions relative to the electricity they produce. If a company outperforms their benchmark, they will be allocated tradable credits. Critics have pointed out the risks of this approach, as the lack of a hard cap and absolute emission reduction targets does not incentivise a transition away from coal, only to a more efficient use of coal. Chinese policymakers do, however, intend to gradually minimise the presence of coal in the country’s energy mix, by lowering price ceilings and cutting back on the credits that can be allocated.

Given the focus on carbon intensity reduction, and in the name of remaining cost-efficient and reliant on market dynamics, the Chinese government does not wish to phase out coal entirely. The goal, rather, is to retire inefficient plants before the end of their expected lifetimes, and retrofit existing plants for carbon capture, storage and reutilisation systems. The credit system has been designed to redirect investments into new and more efficient plants, expediting the transition of capital and human resources away from aging, inefficient plants.

In the short term, a national carbon trading scheme in China will incentivise coal-fired plants to improve plant efficiency or burn higher quality fuel. In the long-term, as alternative energy sources become more widespread and affordable, the aim will be to phase out inefficient and outdated plants altogether.

China’s Bureaucracy and Environmental Policy

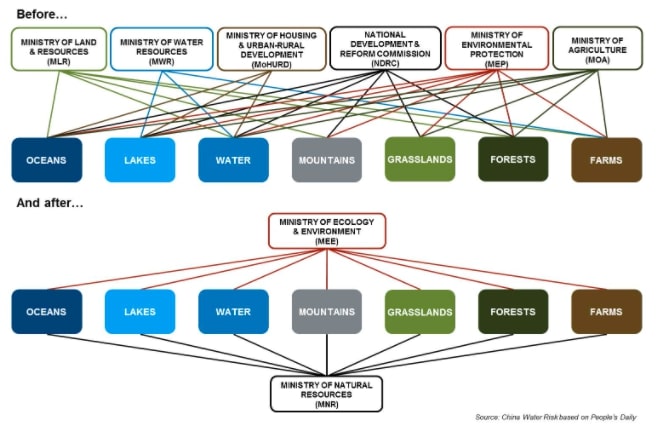

The Chinese government has generally viewed the impacts of climate change through a macroeconomic lens. Historically, climate change policy in China has been devised by the National Development and Reform Commission (NDRC), an institutional body for macroeconomic management, tasked with devising economic and social development policy. The NDRC is a massively influential body in Chinese politics, and climate activists have largely been in favour of having an important and relevant body tasked with combating climate change.

The NDRC played a significant role in devising China’s first carbon trading pilot programmes in 2011, by framing the relevant policy and selecting the participating localities. In 2014, the NDRC issued a set of measures that established a preliminary legal framework for a national carbon trading system. Over subsequent years, NDRC officials continued to tout the eventuality of a national system, and the body was viewed as playing a critical role in the system’s planning.

In 2018, however, as part of a major governmental reshuffle, duties related to climate change policy were stripped from the NDRC, and passed on to a newly formed cabinet body, the Ministry of Ecology and Environment (MEE). Under the jurisdiction of the NDRC, climate change had become categorised as a strictly economic and developmental issue, dispersing environmental policymaking duties and causing serious bureaucratic inefficiencies and difficulties in coordinating environmental policy.

As Zhou Shengxian, China’s former Environment Minister, stated in 2013: “We take care of carbon monoxide, while carbon dioxide falls under the National Development and Reform Commission.”

The reform policies streamlined a very fragmented approach to drafting environmental policy in China. When the NDRC formulated policy on issues pertaining to climate change, other key inputs to the environmental policymaking process were dispersed throughout Chinese politics’ bureaucracy, requiring the NDRC to coordinate exhaustively with multiple other agencies and institutions of China’s intricate machinery of state. The government hopes to improve efficiency by assigning all duties related to environmental policy to the MEE.

The multiple delays in formalising the national carbon trading scheme in China, which had at first been ambitiously slated to begin in 2017, were in large part due to bureaucratic inefficiencies at the policymaking level. One of the major challenges was organising an efficient and reliable data collection system that could indicate baseline emission rates across multiple sectors. This was necessary to establish targets and to efficiently allocate allowances. A more streamlined and coordinated approach to environmental policy through the MEE may reduce the latencies of China’s prior environmental policymaking model.

There remain some concerns over the MEE and its future role. Critics believe that moving climate change-related responsibilities from a massively influential policymaking body such as the NDRC to a smaller and newly formed ministry organism may limit climate change and other environmental issues’ visibility at national policymaking discussions. So far, the national scheme does not appear to have suffered significantly from the governmental reshuffle, other than being delayed. The Chinese state will need to ensure that climate policy remains a priority for legislators in future socio-economic planning.

Systemic Obstacles to a Market-Based Approach

A major difference between China ’s approach to implementing a national carbon trading scheme and those in Western countries lies in the nature of respective structural impediments. For systems established in the EU, for instance, action was challenged by the opposition of industry actors and other stakeholders. Adjusting the market to account for carbon trading was not an insurmountable challenge when compared to the political resistance of powerful lobbyists and industry representatives.

The Chinese government will presumably not encounter substantial political resistance, given the collectivist view on policy that the country’s leaders share. Additionally, many of the highest emitting industries in China, particularly in the power and steel sectors, are state-owned enterprises, virtually eliminating the risks and delays to legislation caused by industry lobbying.

The Chinese government however, faces an altogether different type of challenge. How can a country, which has prided its growth over 40 years on the virtues of a planned and top-down system of economic governance, introduce market-based incentives as the driving factor behind policy outcomes in the span of just a few years?

Despite trends that indicate movement towards a mature market economy, this transition has not been completed, nor do the country’s leaders express any desire to do so. At its core, China remains a socialist market economy, in which free markets and private property only exist within the ubiquitous reach of dominating state-owned enterprises and government actors. This is true in certain sectors more than others, and especially so in the power sector which is largely controlled by firms closely affiliated with the state.

Larry Goulder, a Stanford University economist who has worked on establishing carbon markets in California and Guangdong, said in 2017:

“In China, it’s not explicit political challenges that one faces as much as institutional. That is to say, the country doesn’t have as much of an apparatus for monitoring and keeping track of emissions. In addition, much of the economy is still not a market economy, but rather state-run in terms of the way prices are set, and that’s particularly true of the power sector. One of the key challenges is how to introduce environmental regulations, even market-based regulations, in a world where many of the sectors won’t respond as well because prices are controlled.”

The Chinese government has made it clear that market forces will play a key role in determining the dynamics of a national carbon market, although allowing markets full control over sectors that have historically been dominated by the heavy hand of government presents a significant challenge.

To move towards market-oriented regulating mechanisms, the Chinese state has gradually been enacting relevant reforms. In 2012, the state passed a bill to reform coal pricing. The bill allowed all prices of coal commodities, which had previously been split between state and market determination depending on the buyer and intended use, to be determined by market forces.

Pegging single unit prices to other commodities directed by market dynamics has also been a successful strategy. The case of natural gas is a good example. Historically seen as a lesser fuel source to coal, state agencies have long priced natural gas significantly below production costs, discouraging domestic producers from investing in gas production and restraining imports. Natural gas’ resurgence as a relatively clean alternative to coal, however, led to the introduction of a new pricing mechanism in 2011 by the NDRC, that pegs the per-unit price of natural gas to the price of other alternative fuels that are determined through market forces. This mechanism allows gas prices to be determined according to the market developments of other alternative fuels, gradually decoupling natural gas from years of state price controls and allowing the industry and related infrastructures to grow in China and supplant inefficient coal plants. This pricing mechanism was employed to positive results in some of the pilot trading programmes’ markets.

China has put in motion a series of reforms to decouple prices and resource demand from state interventions, relying increasingly on market forces. For a national carbon market to operate self-sufficiently within a free market environment, these steps are critical. Chinese companies, however, remain in uncharted waters for the most part, and will need to be guided by occasional state intervention. Price floors on carbon trading will be important to implement and adjust when needed, to motivate investor participation and an active market environment. Likewise, price ceilings can limit any single firm or enterprise from gaining disproportionate levels of size and power. Environmental taxes and penalties should not be discounted either, should competition ever need to be balanced out.

The state will need to strike a delicate balance between interventionism and allowing the market to govern itself, between encouraging competition and ensuring a level playing field. China already possesses a wealth of experience from its pilot programmes, as well as important advisory inputs from other carbon trading markets in the world. China’s centralised political system is an advantage, in that the state will not need to worry about combative non-compliance, obstructionist industry lobbying or contesting political priorities. For decades, China’s rapid growth has benefited from coherent policy through command-style economic planning, and the development opportunities afforded by free market capitalism. If the state can balance these two ideologies, it can certainly stake a strong claim as a global leader in market-driven environmental action.

Featured image by: Flickr