Crypto – often used as an umbrella term that encompasses all things cryptocurrency – has received significant and polarising attention over the past decade. Now, industry leaders have entered the carbon trading market with claims that taking these markets onto the blockchain could result in huge gains in environmentally friendly business approaches. But sceptics are unsure just what problem crypto is trying to solve and whether it will be successful in re-energising the carbon credit market as countries race towards net-zero goals.

—

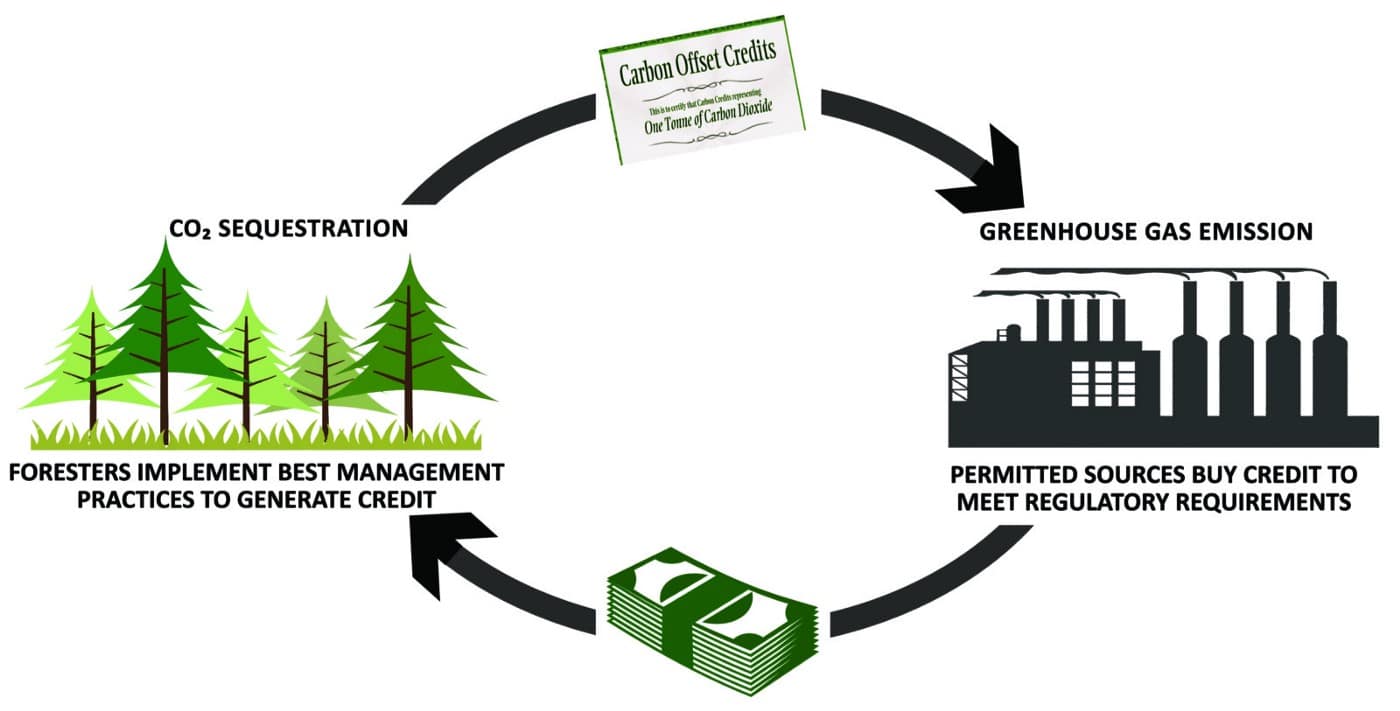

What are carbon credits?

Carbon trading – or the carbon market – was first developed and introduced in the 1990s. In assigning a cost to the environmental damage of CO2 emissions, companies could, in theory, track and offset their own emissions. By purchasing carbon credits tied to ‘green projects’ in the marketplace, businesses across a range of industries could continue their practices while offsetting emissions and therefore reducing environmental damage.

For example, a mining company subjected to an emissions limit could purchase an offset credit owned by a forest owner who could agree to use that money to delay or reduce a harvest. This would then allow the mining company to pollute above their set limit, and use the avoided forest emissions as credit.

Figure 1: The Mechanism of Carbon Offset Credits

Now almost three decades after the introduction of the carbon market, policymakers and activists are unsure of its success. The market remains largely unregulated and discussions are often centred around which projects are counted for inclusion. In fact, several recent studies have highlighted that often, the associated projects are overvalued or have little to no positive impact on the environment. In fact, one study of California forest carbon offsets (worth more than US$2 billion, and the largest programme in the United States) found that almost one-third of all the offsets were over-credited. In total, this amounted to almost 30 million tonnes extra of CO2 emissions.

You Might Also Like: What Are Carbon Credits And How Do They Work?

This problem of over-crediting has left critics of the carbon market frustrated. A combination of a lack of transparency and a systematic flaw in the way that these credits are calculated has ensured that projects are continually miscalculating both the pollutant emissions and the emissions saved.

Taking the study of California as an example, there are often big misconceptions about what constitutes an environmentally friendly offset project. The vast majority of these projects do not involve the growth of new forests as it is often believed but are instead devoted to the development of practices known as ‘Improved Forest Management’ (IFM), which are considerably more incremental in the environmental benefits. Just this one example highlights some of the problems with carbon markets and their oftentimes exaggerated utility.

Double counting – a term that refers to a situation in which two separate parties claim the same carbon removal project or credit – has also emerged as a problem with the current carbon market. It is indeed a considerable problem and has highlighted the gap between the theory and practice of carbon markets. So how does this happen?

Most commonly, double counting happens when both the organisation offsetting the emissions and the host country of the project aiming to reach climate goals under the Paris Agreement claim the credits. This is obviously problematic: both a country and a company are claiming to be carbon neutral and yet, in terms of emissions reductions, nothing has actually been achieved. Beyond the immediate environmental effects, double counting also disincentivizes countries to take action to meet climate goals in the long term.

How Does Crypto Fit Into Carbon Markets?

Crypto proponents believe that a solution lies in this carbon marketplace. Industry leaders have argued that the traditional carbon market is outdated, disorganised, and often lacking in incentives. They suggest that by moving carbon credits onto the blockchain – a digital and open database – that crypto-economics could incentivise businesses to adopt more environmentally friendly approaches.

Additionally, crypto traders argue that if more people got involved in crypto carbon credits, this would drive the price of credits up. In doing so, they hope to force companies to pay higher prices for emissions reduction or drive them to invest in more energy-efficient business practices.

The starting approach from the crypto industry was to ‘sweep the floor’. This involved using a bridging process to purchase carbon credits that were already in circulation in the conventional market and migrate them to the blockchain, at which point a token would be issued to the owner. These tokens can then serve as tradable objects through which trading on the blockchain can take place. Although proponents of such a transfer to the blockchain often tie their mission to environmental goals, there is a clear financial incentive to the transfer. In the current marketplace, the price of carbon offset credits has traded in the range of US$1-2. There are also financial incentives to convert the Base Carbon Tokens (BCT) to KLIMA tokens; in the initial stages market prices for such tokens surged to a high of over $3000, demonstrating a clear profit for those involved.

While in theory, the open-access blockchain technology provides increased transparency, an analysis of some of the first crypto carbon credits issued revealed two striking findings. The first was that a significant number of ‘zombie’ projects – projects that were not active until the economic incentives generated by crypto carbon credits were generated – had appeared on the blockchain. The second was that nearly all of the credits that had migrated to the blockchain through the Toucan protocol came from projects that had originally been excluded from the current carbon market because of concerns about the quality of the project. So what do these two findings mean for climate action?

What Are the Weaknesses of Crypto Carbon Credits?

The appearance of ‘zombie’ projects might initially sound positive. In theory, more projects for carbon offsetting should lead to a decrease in emissions. But often, if these credits aren’t finding buyers on the traditional carbon market, it is because buyers had concerns about the quality of the projects in the first place. By migrating these credits onto the blockchain, those concerns are not addressed. Instead, previously unsellable credits and projects are simply being used for revenue generation by the owners who “swept the floor” rather than the generation of new, exciting projects with real potential. But these projects are not the only credits of concern.

The Paris Agreement laid out regulations for the carbon market in the rules for trading Clean Development Mechanism under Article 12, which prohibits the trading of credits before January 2013. This is to ensure that any new carbon offset claims are in line with revised standards. However, a staggering 84.8% of crypto carbon credits that were being traded would not have met the Paris Agreement regulations, as they were registered before 2013. In short, crypto carbon credits simply appear to be trading projects that would not have found buyers in the conventional markets. In doing so, this technology only serves to amplify existing structural problems within the current carbon market while avoiding regulatory standards put in place under the Paris Agreement.

Crypto proponents claim that the advantage of migrating to the blockchain would be to tackle an outdated, non-transparent, and disorganised carbon market. In doing so, they hope to either drive the price up on carbon emissions or force companies to search for more energy-efficient practices. While it is true that the price may have been driven up for some credits, these appear to have benefited the owners of the credits; whereas the environmental benefits to this practice are either negligible or, in some cases, have been even made worse.

But if crypto isn’t the answer to the carbon market’s problems, what is?

Can We Fix the Current Carbon Market Without Crypto?

To address the significant problem of double counting, adjusting the national emissions targets in Article 12 was a good first step. This meant implementing a policy on the hotly contested ‘corresponding adjustments’. These adjustments mean that the CO2 emissions reduced or removed by the offsetter will be deducted from the greenhouse gas inventory of the project country. This mechanism ensures that for each carbon credit that is purchased on the market, only one country is claiming the emissions reduction.

Ultimately, the biggest problem with carbon credits is the lack of a single standard of quality. This means that there is a high likelihood that many sub-optimal projects end up being priced and traded even if there is no benefit to the environment. If markets want to be serious about changes to climate change, there has to be a move away from the funding of small, individual projects and toward paying entire companies and therefore whole industries, to reduce emissions. Ultimately, crypto encouraged the funding of these smaller, negligible, and oftentimes defunct projects which is counter to solutions suggested by experts.

To have a single standard of quality, a reliable and verifiable benchmark for emissions reduction has to be put in place. In targeting individual companies and then industries as a whole, both voluntary and offset markets could be improved as the world aims for a low-carbon future.

You Might Also Like: How Tokenized Carbon Credits Could Help Advance Climate Solutions