With the Federal government proposing big policy initiatives for the US in 2022, it is worth considering Green Quantitative Easing (Green QE) as an alternative route to economic recovery in the aftermath of the COVID-19 pandemic. But how did we get here and what does this all mean?

—

Throughout the last two years, you may have noticed your cost of living has increased significantly, perhaps it’s your weekly groceries expense or the cost of getting something delivered to your house. But even though you are paying more, your quality of life doesn’t seem to be increasing, this phenomenon in technical terms is known as inflation.

While it is true that the price increase is due to labour shortage caused by COVID-19, it’s also an unintentional side effect of “quantitative easing”, and right now, the government is going to “taper” to fix the underlying issue. But what does these two terms even mean, what did the US government do last year that’s causing inflation, and how can Green Quantitative Easing potentially fix all this?

What Is Quantitative Easing and Tapering?

To people outside of finance and economics, these concepts may be a bit foreign, as the financial field tends to complicate simple ideas. To understand quantitative easing (QE) and tapering, let’s see what happened during the pandemic.

At the beginning of the pandemic, most people expected the shutdown was going to be short term, but the contagious nature of the virus has extended the stay-at-home order across the world. We witnessed borders between countries closed or restricted, shops and restaurants shut, with many people losing their jobs; essentially the entire world came to a halt.

To prevent a recession from the lack of economic activities, many national governments adopted a series of economic policies known as quantitative easing or QE for short. The textbook definition of QE is boring and full of jargons, possibly intentionally so as to make this field appear more complicated than it is. QE by definition is a form of expansionary monetary policy where central purchases of bonds and financial assets stimulate economic activity.

To oversimplify, the government is essentially printing and injecting money into the economy, increasing the overall money supply, and thus expanding economic activities. This is why stimulus checks were given out throughout the past two years in many countries as a way to encourage people to spend that money and support local businesses. However, because of the law of supply and demand, the more abundant something is, the less valuable it is. In this case, because there is an abundance of money circulating the world, the worth of money itself decreased.

So then, what is tapering? Tapering is in fact, the opposite of QE. Now that the economy is recovering with the virus slowing down and vaccines are rolling out, the government is trying to reduce the amount of money circulating in the economy.

Why Taper?

While scholars in the field of economics may argue the effectiveness of QE policy, the general consensus is that QE can mitigate the impact of an economic recession triggered by unforeseeable events as in the case of COVID-19. However, the practice of QE has some inherent side effects, among which is inflation.

Inflation itself may not necessarily be bad, in fact, mainstream economists believe a healthy amount of inflation is good. This is because inflation makes things more expensive over time, thus incentivising spending instead of saving money, therefore boosting the economy. As such, governments around the world try to target annual inflation at around 2%.

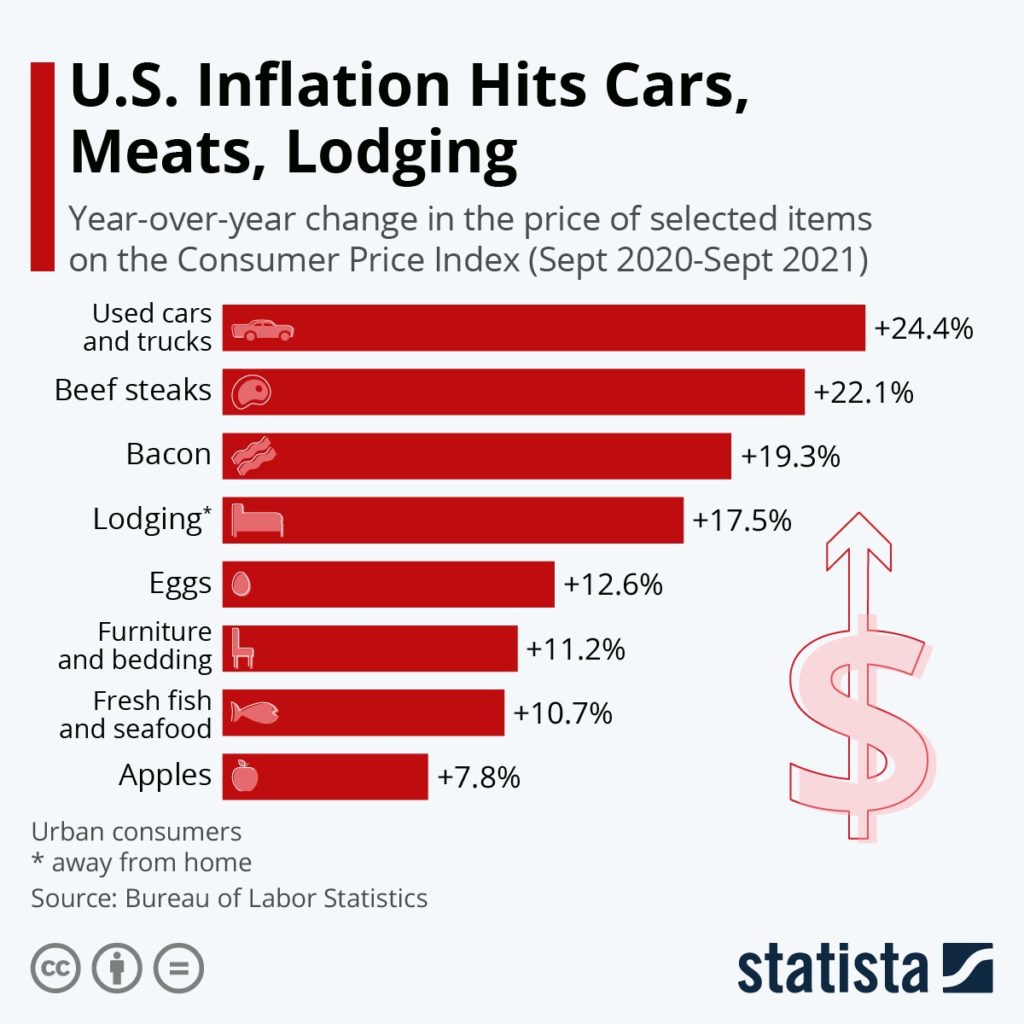

However, throughout 2021, several economic indicators have suggested that we are currently experiencing higher inflation than pre-COVID era. For example, the Personal Consumption Expenditures index (PCE) in the US, which tracks consumer spending, increased 4.3% in August compared to a year ago, which is reflected from the surge of energy and food prices. Below is a graph that provides an overview of inflation across different areas of spending.

Nonetheless, the US federal government continues to suggest that inflation is transitory, that is to suggest that inflation is a temporary situation and will soon recover to its target rate. There is some validity to this statement; currently, the world is experiencing global supply chain issues, largely due to the backlog caused by the surge of demand in the aftermath of COVID-19, and it is only compounded by a shortage of workers at the moment. Regardless, the price surge is apparent and it is higher than expected at the moment.

You might also like: Could the Next Financial Crisis Involve a Carbon Bubble?

The Dilemma

Right now, the federal government is facing quite a dilemma on the topic of QE and tapering. And that is how to stop QE and initiate tapering without tanking the economy. To understand this, we need to ask where did the money for QE go?

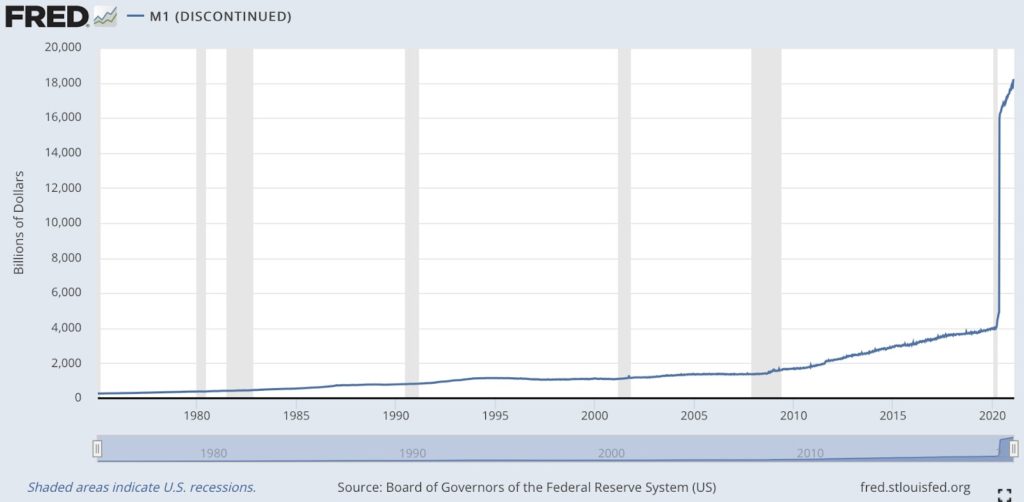

Supposedly, the money for QE should’ve returned to the economy, it is certain that some of that money did help individuals pay rent or help businesses stay afloat. It is estimated that 40% of all US dollars in existence were printed between May of 2020 to May of 2021. If we look at the most recent money supply graph below, the figure is even more staggering.

Yet in spite of this, we don’t see the same level of economic recovery, so where did the money go? Some experts suggest that this money is reflected in the inflated stock market or other investments. If we look at the S&P 500 as an overall indicator of the stock market’s performance, we will notice that since the big financial crash of March 2020, it has returned to 98% of pre-pandemic levels as of October of 2021. Another area where this money might’ve gone is real estate and crypto currencies. The former has grown significantly throughout last year and the latter reached historically high levels of investment in April 2020. In summary, the current market, both in real life and in the stock market, is highly inflated.

The US government is in a tough spot at the moment. On the one hand, they want to continue to use QE to assist economic recovery, but they fear that inflation may eat away the middle class. On the other hand, if they taper, it can help with inflation, but it may slow down growth and tank the stock market.

Green Quantitative Easing: the Alternative Path?

Clearly from this, we can see that the conventional QE has its inherent weaknesses. The belief that the so-called invisible hand will efficiently allocate the money is simply not true. The way that QE injects money into the economy indiscriminately means that it misses out on opportunities to fund green projects that could provide structural transition to the current economy. Ultimately, the issue centres on the fact that money didn’t trickle down to areas where it matters to ensure a healthy recovery. Fortunately, we have an alternative road we can take: Green Quantitative Easing.

In 2015, Jeremy Corbyn, a democratic socialist and former leader of the Labour Party, proposed the idea of People’s Quantitative Easing. The scheme initially aims to address the UK’s labour productivity issue, creating provisions that can “meet future needs, whether it be in infrastructure, innovation or business capacity.” Later, this concept was modified and further developed into Green Quantitative Easing by Richard Murphy, political economist and the director of Tax Research UK. For Green QE, instead of relying on the financial market to direct that newly injected money, the central bank will “buy debt not principally from the banks but instead from private sector businesses, local and regional governments, and social enterprises, where those organisations can demonstrate that the central bank’s money will be used for green purposes”. In layman’s terms, Green QE ensures that investments are always made directly into the pockets of companies with verified green objectives.

Green QE essentially allows several things to happen together. As previously mentioned, currently the government is in a tough spot in determining how to taper without tanking the economy and halt recovery. With Green QE, the government can continue injecting money into the economy albeit in a more selective manner, but it mitigates the fear of slowing down the economy while it is recovering.

Second, under this scheme, the central bank partners with the private sector and invests directly in companies that “intend to fund projects on energy efficiency, renewables and any other type of environmentally friendly investment”. What this can achieve is prevent the misallocation of resources and alleviate the issue of how conventional QE inflated equity prices in the stock market. Green QE encourages investment for cleaner infrastructure by reducing the cost of borrowing for these projects. In addition, given that the green sector tends to be more labour intensive, as in the case of organic farming which requires 32% more workers, it is likely that Green QE will have a positive effect on net-employment.